Award-winning PDF software

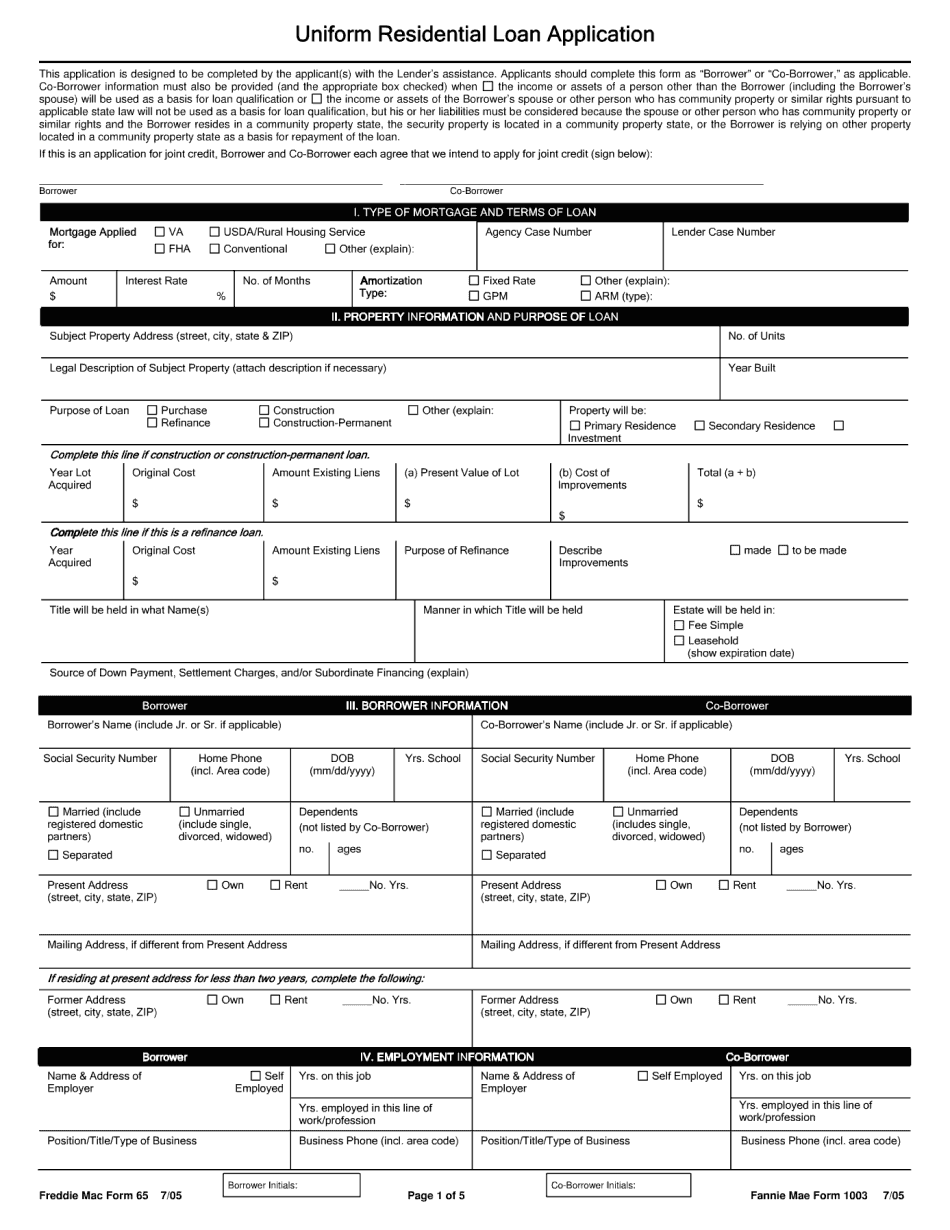

Uniform residential loan application (form 1003) | fannie mae

The new spec states that the borrower will be required to furnish any and all required disclosures on the Application, including the title, monthly payment, down payment, closing cost, and monthly cost of borrowing. The spec gives borrowers until noon today (September 26) to file their 1003, which is just two weeks away. The spec also says that if the borrower does not file the 1003, it will create no right of return or any right of reimbursement to the borrower for the loan. Borrowers will face a late fee, which is an increase from last year, and a 100% closing cost fee with the addition of a 10% fee for “unusual payment patterns.” The origination fee (which covers the fees associated with filing an application) will change to 1,000 per loan, up from no fee on originations in 2014. The new spec also prohibits “any attempt to increase the loan amount or the.

uniform residential loan application - fannie mae

LN) Lender name (name of lender) Lender address with ZIP code Lender type Fannie Mae Federal Housing Administration Federal Housing Administration (the “FSA”; also referred to as the Fannie Mae FHA) Federal Home Loan Bank of New York (FLB; also referred to as “FLB”) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Lender type (name of the borrower) (address) Lender type (name of the borrower) (address) Lender type (name of borrower) (address) Lender type (name of borrower) (address) Mortgage Purchase Agreement and Home Equity Line of Credit (MONA) Agreement Form, or (MONA Form 50) Married Couple MA Agreement and Home Equity Line of Credit (MONA) Form. To be completed by the Lender: Lender Loan No. (LN) Lender name (name of lender) Lender address.

instructions for completing the uniform residential loan application

The Federal Housing Administration has updated their website, and provides a detailed description of their new guidelines for homeownership counseling. 3. The United States Office of Thrift Supervision has released their new homeownership counseling guidelines. You can find more information at: 4. The US Department of Housing and Urban Development has released a pamphlet, “Choosing to Buy Home”: A Homebuyer's Guide to Protecting Your Capital. See also: 5. The Federal Housing Finance Agency (FIFA) has released their updated homeownership guidelines. See also: 6. If you live in a building with 25+ units, you may be able to get a Section 203 mortgage. 7. Mortgage-backed securities have become the new normal in the mortgage market. The FIFA has recommended the use of mortgage-backed securities as a way to raise funding to stabilize the mortgage market and protect taxpayers from mortgage defaults. It is possible that you want to use.

redesigned uniform residential loan application (form 1003)

As part of its mortgage industry reform plans, HUD (which oversees Fannie Mae and Freddie Mac) changed some mortgage credit standards as required by the Dodd-Frank Regulation and Related Agencies Act (the Dodd-Frank Act). The first thing you need to know about the Dodd-Frank changes is that they are a “consensus change” across all mortgage credit programs: all of Fannie Mae and Freddie Mac's mortgage products, as well as all of its loan products. That means that if this reform plan was to really make a dent in the massive amounts of credit card debt that Americans are currently carrying, it would cost the federal government billions of dollars for those agencies to implement the changes. The reforms are a “consensus change, and the agencies will work with other federal agencies to implement and manage the new standards.” As I wrote in the December 22 post Housing Reform Is a.

uniform residential loan application interactive (form 1003): pdf

Lenders can provide additional information regarding the application process, including the amount of the loans to be forgiven. Applications for this type of loan may also be prepared by a non-refundable prepaid debit card and submitted with a separate application. Loan relief will not be granted during the early application/interview process. NOTE: The Lenders can cancel the application at any time. Should you need immediate help, please call. If you need emergency assistance, please call the non-emergency number that corresponds to your state.